Updated: May 2026An insurance broker is a licensed insurance professional who helps businesses compare, arrange and manage insurance. For tradies, contractors and business owners, a broker can help identify the types of cover that may be relevant, explain policy options in plain English and support you with certificates, renewals and claims.

Unlike buying direct from one insurer, an insurance broker can approach a range of insurers and underwriting agencies to find policy options that suit your trade, contracts, work sites, equipment and business structure. Cover remains subject to policy terms, conditions, limits, exclusions and insurer acceptance.

Quick Summary

- An insurance broker helps you understand, compare and arrange insurance based on your business risks and requirements.

- A broker can explain policy options, limits, exclusions, certificates and contract insurance clauses in practical terms.

- For tradies and contractors, brokers commonly assist with Public Liability Insurance, Professional Indemnity Insurance, Property and Tools Insurance, Commercial Vehicle Insurance and other business cover.

- A broker can support clients through the claims process, but the insurer decides whether a claim is accepted under the policy.

- Insurance brokers in Australia must operate under the appropriate licensing and regulatory requirements.

What Does an Insurance Broker Do?

An insurance broker works with you to understand your risks, then helps source insurance options from insurers or underwriting agencies. The broker’s role is to help you make an informed decision, not simply sell you a policy.

For example, a carpenter may need Public Liability Insurance, Property and Tools Insurance, Commercial Vehicle Insurance and Personal Accident and Illness Insurance. A mining contractor may need higher liability limits, plant cover, contract-specific endorsements and Certificates of Currency with particular wording.

An insurance broker can help identify these requirements before a job starts, which can reduce delays with site access, tender submissions and client onboarding.

What Is the Role of an Insurance Broker?

The role of an insurance broker is to help clients arrange and manage insurance in a structured way.

An insurance broker may assist with:

- Understanding your business activities and risk profile

- Identifying insurance types that may be relevant to your business

- Comparing policy options from available insurers and underwriting agencies

- Explaining policy limits, exclusions, excesses and conditions

- Reviewing contract insurance requirements

- Helping arrange Certificates of Currency where available

- Checking whether policy wording aligns with your business activities

- Coordinating renewals and policy updates

- Helping update cover when your business changes

- Supporting clients through the claims process

- Helping communicate with insurers during a claim

- Providing general insurance information and guidance

A broker does not control claim outcomes. Claims are assessed by the insurer based on the policy wording, circumstances, exclusions and supporting evidence.

Why Tradies and Contractors Use Insurance Brokers

Tradies and contractors often use insurance brokers because trade insurance can become complicated quickly. A basic policy may not address site access rules, subcontractor structures, principal contractor requirements, plant risks, tools in transit or contract-specific clauses.

A broker can help make these details easier to manage.

This is particularly useful if you:

- Need a Certificate of Currency urgently for site access

- Work across multiple sites or project types

- Use subcontractors or labour hire

- Own expensive tools, vehicles, plant or machinery

- Work under builder, mining, civil or government contracts

- Need to meet insurance clauses before signing a contract

- Have had a claim or insurance issue before

- Are unsure whether your current policy reflects your actual work

For many trades, the risk is not just whether insurance is in place. The bigger issue is whether the policy is structured around the work being performed.

Insurance Broker vs Insurance Company

The main difference between an insurance broker and an insurance company is who they work with and what they can offer.

| Area | Insurance Broker | Insurance Company |

|---|---|---|

| Role | Helps clients compare and arrange insurance options. | Provides insurance products issued by that insurer. |

| Market access | Can often approach multiple insurers or underwriting agencies. | Usually offers its own products only. |

| Policy guidance | Can explain differences between available policy options. | Explains its own products and policy terms. |

| Claims support | Can support clients through the claims process. | Assesses claims under the policy. |

| Best suited for | Businesses with contract requirements, trade risks or multiple cover needs. | Simple insurance needs where one insurer’s product is suitable. |

Both brokers and insurers have a role in the insurance process. For trades, construction, mining and heavy industry businesses, using a broker can be helpful when the insurance requirements are more detailed or time-sensitive.

What Insurance Can a Broker Help Arrange?

An insurance broker can help arrange many types of business insurance, depending on the client’s industry, risk profile and insurer appetite.

For tradies, contractors and SMEs, this may include:

- Public Liability Insurance

- Professional Indemnity Insurance

- Property and Tools Insurance

- Commercial Vehicle Insurance

- Contract Works Insurance

- Plant and Machinery Insurance

- Business Package Insurance

- Personal Accident and Illness Insurance

- Workers Compensation Insurance, where available and subject to state licensing restrictions

- Management Liability Insurance

- Cyber Insurance

Not every business needs every policy. The right setup depends on what the business does, who it works for, what assets it owns and what the contract requires.

How an Insurance Broker Helps With Contracts

Contract insurance clauses can be difficult to read if you are not dealing with them every day. A broker can help review the insurance section of a contract and explain what the client, builder, principal contractor or landlord is asking for.

Common contract insurance requirements include:

- Minimum Public Liability Insurance limits

- Professional Indemnity Insurance for design, advice or consulting work

- Contract Works Insurance for construction projects

- Workers Compensation Insurance requirements

- Principal indemnity wording

- Waiver of subrogation clauses

- Cross liability clauses

- Interested party requirements

- Specific Certificates of Currency before work starts

These clauses are not always automatically covered by a standard policy. A broker can help check whether the requirement can be met under the available policy options. Any changes, endorsements or certificate wording are subject to insurer acceptance.

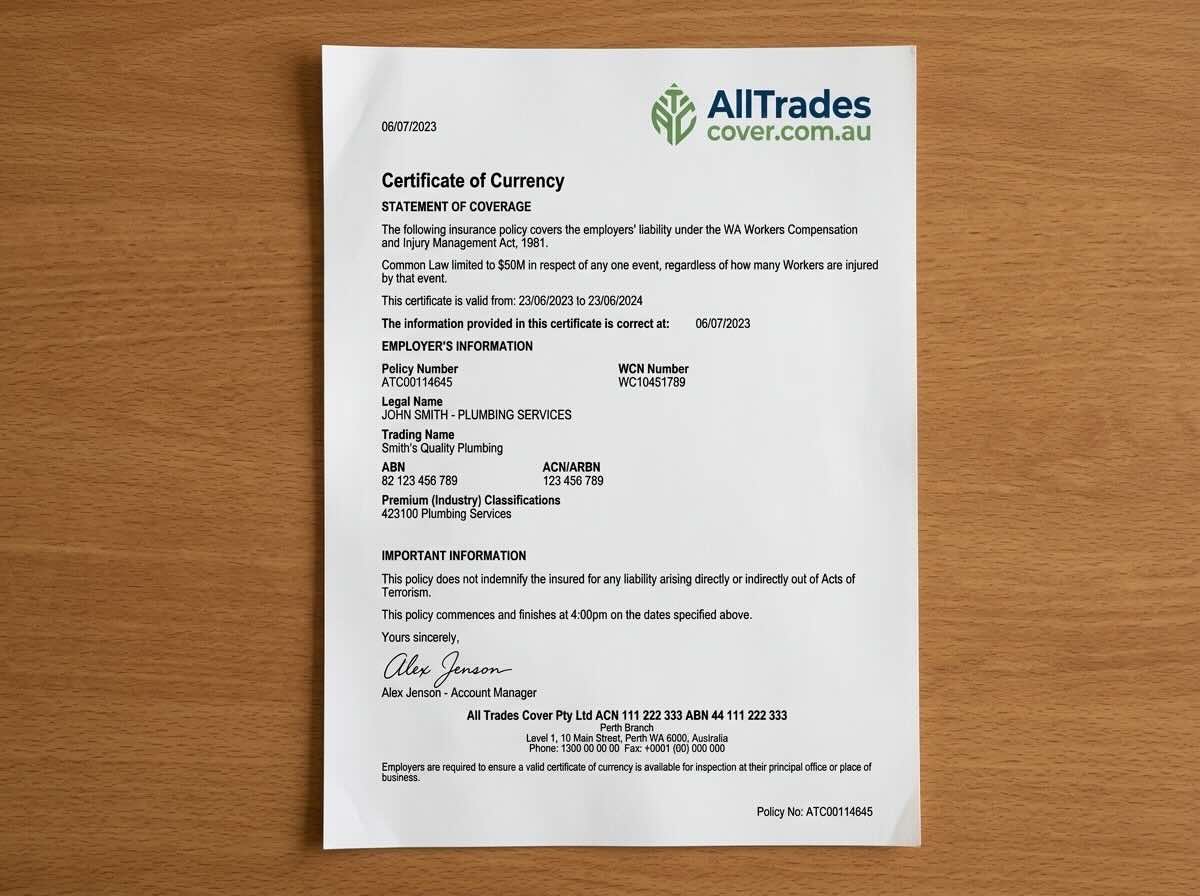

How an Insurance Broker Helps With Certificates of Currency

A Certificate of Currency is often required before a tradie or contractor can start work. It confirms that an insurance policy is current at the date the certificate is issued.

An insurance broker can help arrange Certificates of Currency where available and check whether the details match the request.

This may include checking:

- The insured business name

- The policy type

- The policy limit

- The policy expiry date

- The business activities listed

- Interested parties, where accepted by the insurer

- Contract-specific wording, where accepted by the insurer

This can be useful when a builder, principal contractor, council, landlord or lender needs proof of cover before approving work, access or finance.

How an Insurance Broker Helps at Claim Time

An insurance broker can support clients through the claims process by helping gather information, submit forms and communicate with the insurer.

This support may include:

- Explaining what information the insurer may need

- Helping complete claim forms

- Assisting with documents, photos, invoices and incident details

- Communicating with the insurer or claims team

- Helping clarify policy wording and insurer questions

- Keeping the client informed during the process

The insurer is responsible for assessing the claim. A broker can assist with the process, but cannot guarantee that a claim will be accepted or paid.

Do Insurance Brokers Save Money?

An insurance broker may help you compare available policy options and pricing, but the cheapest premium is not always the right result.

A lower-cost policy may have narrower wording, lower limits, higher excesses or exclusions that do not suit your work. For a tradie, contractor or business owner, value often means finding a policy that aligns with your actual risks and contract requirements, not just choosing the lowest price.

A broker can help explain the difference between policy options so you can make a more informed decision.

Do Insurance Brokers Need Qualifications?

Insurance brokers in Australia must operate under the appropriate licensing and regulatory framework. This often involves working under an Australian Financial Services Licence, meeting training requirements and following professional conduct obligations.

Many brokers also complete ongoing professional development to maintain their technical knowledge. This matters because insurance can be complex, especially when policies need to respond to trade, construction, mining, civil or commercial risks.

All Trades Cover holds AFSL 418512 and works with trades, construction, mining and heavy industry businesses across Australia.

When Should You Speak to an Insurance Broker?

You should consider speaking to an insurance broker when your insurance needs are more detailed than a simple online policy purchase.

This may include when you:

- Start a new trade or contracting business

- Need insurance to win or start a job

- Receive a contract with insurance clauses

- Need a Certificate of Currency urgently

- Buy new tools, machinery, plant or vehicles

- Start hiring employees or subcontractors

- Move into commercial premises

- Take on larger or higher-risk projects

- Expand into mining, civil, government or commercial work

- Have a claim or insurer dispute

- Need to review whether your current policy still suits your business

Insurance should be reviewed as your business changes. A policy that worked when you were a sole trader may not be suitable once you employ staff, add vehicles, take on subcontractors or sign larger contracts.

Why Work With All Trades Cover?

All Trades Cover is a specialist insurance brokerage for trades, construction, mining and heavy industry. We work with tradies, subcontractors, builders, plant operators, mining contractors and SMEs that need insurance arranged around real business risks.

We can help with:

- Trade-specific insurance options

- Fast quotes and Certificates of Currency where available

- Contract insurance clause reviews

- Policy comparisons from trade and construction insurers

- Public Liability Insurance, tools cover, vehicles, plant, contract works and more

- Claims support and insurer communication

- Insurance reviews as your business grows

Our role is to help make insurance clearer and more practical, so you can understand your options before choosing cover.

Frequently Asked Questions

What Is an Insurance Broker?

An insurance broker is a licensed insurance professional who helps clients understand, compare, arrange and manage insurance. A broker can help explain policy options, review insurance requirements and support clients through renewals and claims.

What Does an Insurance Broker Do for Tradies?

An insurance broker can help tradies arrange cover such as Public Liability Insurance, Property and Tools Insurance, Commercial Vehicle Insurance, Personal Accident and Illness Insurance and other business policies. The broker can also assist with Certificates of Currency and contract requirements.

Is an Insurance Broker the Same as an Insurer?

No. An insurer issues the insurance policy and assesses claims under the policy. A broker helps the client compare, arrange and manage insurance options.

Can an Insurance Broker Help With Claims?

Yes. An insurance broker can support clients through the claims process by helping with paperwork, communication and claim information. The insurer decides whether the claim is accepted under the policy.

Can an Insurance Broker Get Me the Cheapest Policy?

An insurance broker can compare available pricing and policy options, but the cheapest policy may not be the most suitable option. A broker can help explain what is included, what is excluded and how the policy fits your business risks.

Do I Need an Insurance Broker for Public Liability Insurance?

You do not always need a broker to buy Public Liability Insurance, but a broker can be helpful if you have contract requirements, site access conditions, higher-risk work, subcontractors or questions about policy wording.

Can a Broker Help With a Certificate of Currency?

Yes. A broker can help arrange a Certificate of Currency where available and check whether the certificate details match the client, builder, lender or site requirement.

How Is an Insurance Broker Paid?

Insurance brokers may be paid by commission, fees or a combination of both. The broker should explain relevant costs, commissions or fees in line with their disclosure obligations.

When Should I Contact an Insurance Broker?

You should consider contacting a broker before signing a contract, starting a new business, entering a worksite, hiring staff, buying major equipment or renewing a policy that may no longer match your business.

Does All Trades Cover Only Work With Tradies?

All Trades Cover specialises in trades, construction, mining and heavy industry, but may also assist SMEs with business insurance needs. Whether cover can be arranged depends on the business activity, insurer appetite and underwriting requirements.

Speak to an Insurance Broker Who Understands Trade Risk

If you are a tradie, contractor, builder, plant operator or business owner, All Trades Cover can help you understand your insurance options and arrange cover that reflects your work, contracts and business structure.

To discuss your insurance needs, contact All Trades Cover on 1300 826 850 or complete our online quote form.

General Advice Warning: This information is general only and does not take into account your objectives, financial situation or needs. Cover is subject to policy terms, conditions, limits, exclusions and insurer acceptance. Before deciding whether a policy is suitable, read the relevant policy wording and consider whether the cover meets your circumstances.