Updated: May 2026

A Certificate of Currency is a document that confirms an insurance policy is current at the date it is issued. It is often requested by clients, builders, principal contractors, lenders, councils, landlords or site managers before a business can start work, access a site or meet contract requirements.

For tradies, contractors and small business owners, a Certificate of Currency is commonly used as proof that a policy is in place for a specific type of insurance, such as Public Liability Insurance, Professional Indemnity Insurance, Contract Works Insurance, Property and Tools Insurance or another business insurance policy.

Quick Summary

- A Certificate of Currency confirms that an insurance policy is current at the time the certificate is issued.

- A Certificate of Currency is not the full insurance policy and does not list every policy term, condition, limit or exclusion.

- Clients, builders, councils, landlords, lenders and principal contractors may request a Certificate of Currency before work starts.

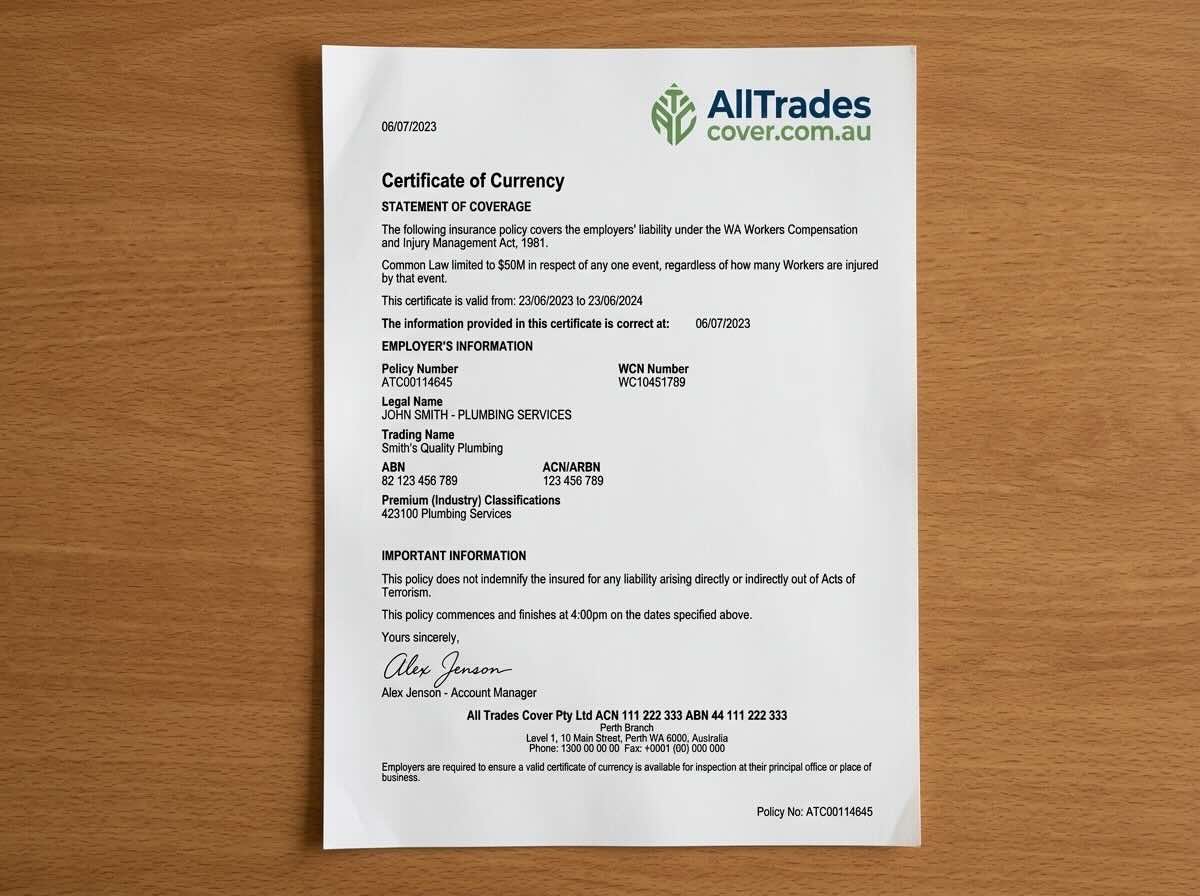

- A Certificate of Currency usually includes the insured name, policy type, policy number, insurer, expiry date, cover limit and interested parties where applicable.

- Cover remains subject to the policy wording, terms, conditions, limits, exclusions and insurer acceptance.

What Does a Certificate of Currency Mean?

A Certificate of Currency means there is a current insurance policy in place for the insured party named on the certificate. It gives the person requesting the document a snapshot of the policy details, including the policy type, policy period and the insured business or individual.

For example, a builder may ask a subcontractor for a Certificate of Currency for Public Liability Insurance before allowing the subcontractor onto a construction site. The certificate helps the builder confirm that the subcontractor has arranged the type of cover required under the site or contract conditions.

A Certificate of Currency does not mean every claim will be accepted. It also does not replace the full Product Disclosure Statement, policy schedule, endorsements or policy wording.

What Information Is on a Certificate of Currency?

Most Certificates of Currency include key policy details that allow another party to check whether the policy appears to meet basic contract, finance or site access requirements.

Common information may include:

- The name of the insured person or business

- The trading name, where applicable

- The insurer or underwriting agency

- The insurance broker, where applicable

- The policy number

- The type of insurance policy

- The policy start date and expiry date

- The limit of indemnity or insured amount

- The insured location, business activity or property, where relevant

- Interested parties, such as a lender, principal contractor, landlord or finance provider, where accepted by the insurer

- Any key endorsements, extensions or notes that the insurer agrees to show on the certificate

The exact information shown depends on the insurer, the policy type and the wording the insurer is prepared to issue.

Why Do Businesses Need a Certificate of Currency?

Businesses often need a Certificate of Currency because another party wants evidence that insurance has been arranged before work, finance, tenancy or site access proceeds.

A Certificate of Currency may be requested when:

- A contractor is starting work on a commercial or residential construction site

- A subcontractor needs to prove Public Liability Insurance before being approved by a builder

- A business is signing a lease for commercial premises

- A lender or finance provider wants to confirm an insured asset is covered

- A council requires proof of insurance before issuing a permit

- A principal contractor needs confirmation of policy limits under a services agreement

- A mining, civil or heavy industry client needs evidence of cover before mobilisation

- A business is tendering for work and needs to show insurance details as part of the submission

- A client needs a certificate before approving an invoice, purchase order or contract start date

For trades and construction businesses, a Certificate of Currency is often a practical document used to keep work moving. Without the certificate, a contractor may not be approved to start a job, even if the policy itself has already been arranged.

Is a Certificate of Currency the Same as an Insurance Policy?

No. A Certificate of Currency is not the same as an insurance policy. It is a summary document that confirms certain policy details at a point in time.

The full policy documents usually include:

- The policy schedule

- The Product Disclosure Statement

- The policy wording

- Any endorsements or special conditions

- Definitions, limits, excesses and exclusions

A Certificate of Currency should be read as evidence that cover is current, not as a full explanation of what the policy may or may not cover. If a client or contractor needs to check whether a policy responds to a specific contract clause, the full policy wording may need to be reviewed.

Certificate of Currency vs Certificate of Insurance

A Certificate of Currency and a Certificate of Insurance are often used to describe similar documents. In many business insurance settings, both terms refer to a document confirming that an insurance policy is current.

The wording can vary between insurers, brokers, lenders and industries. Some parties may specifically ask for a Certificate of Currency, while others may ask for a Certificate of Insurance or proof of insurance.

If a contract uses a specific term, it is worth checking whether the requesting party needs standard evidence of current insurance or a certificate with particular wording, limits, insured activities or interested party details.

What Types of Insurance Can Have a Certificate of Currency?

A Certificate of Currency can be issued for many types of business insurance, depending on the policy and insurer.

Common examples include:

- Public Liability Insurance

- Professional Indemnity Insurance

- Contract Works Insurance

- Property and Tools Insurance

- Commercial Vehicle Insurance

- Plant and Machinery Insurance

- Business Package Insurance

- Workers Compensation Insurance, subject to state rules and insurer arrangements

The certificate should match the policy type requested. For example, if a builder asks for proof of Public Liability Insurance, a certificate for Commercial Vehicle Insurance will usually not satisfy that requirement.

Who Might Ask for a Certificate of Currency?

A Certificate of Currency may be requested by any party that needs to confirm insurance before approving work, finance, site entry or a commercial arrangement.

Common parties include:

- Builders and head contractors

- Principal contractors

- Mining and civil project managers

- Commercial clients

- Government departments and councils

- Property managers and landlords

- Banks, lenders and finance providers

- Equipment finance companies

- Strata managers

- Tender panels and procurement teams

The requesting party may also ask for a specific limit of cover, such as $5 million, $10 million or $20 million Public Liability Insurance. Whether that limit is available or appropriate depends on the policy, insurer appetite, business activities and underwriting acceptance.

Why Contract Wording Matters

Contract wording matters because a Certificate of Currency may need to show more than a basic policy summary. Some contracts require specific limits, interested parties, principal indemnity clauses, waivers of subrogation, cross liability clauses or business activity descriptions.

For example, a subcontractor working under a head contractor may be asked to provide a Certificate of Currency showing the head contractor as an interested party. A mining contractor may need certificate wording that aligns with site access or prequalification requirements.

These requests are not always automatically included. The insurer may need to review and accept the wording before it appears on the certificate. In some cases, the existing policy may need to be amended, endorsed or replaced to meet the contract requirement.

All Trades Cover can help clients review the insurance requirements in a contract and arrange certificate wording where available and accepted by the insurer.

Can a Certificate of Currency Be Updated?

Yes. A Certificate of Currency can usually be updated if the policy changes, renews or needs to show additional accepted details.

A certificate may need to be updated when:

- The policy renews for a new period

- The insured business name changes

- The business adds a new trading name

- The cover limit changes

- A lender, landlord or principal contractor needs to be listed as an interested party

- The business takes on a new contract with different insurance requirements

- The business adds new locations, vehicles, equipment or activities

- The insurer agrees to add contract-specific wording

Any change remains subject to insurer approval and policy terms. A broker can help check whether the requested change can be made under the existing policy.

How Long Is a Certificate of Currency Valid For?

A Certificate of Currency is generally valid while the policy shown on the certificate remains current. Most certificates show a policy start date and expiry date.

The certificate may no longer reflect the current position if the policy is cancelled, changed, replaced or not renewed. This is why some clients ask for a new Certificate of Currency at renewal, even if they already have a copy from the previous policy period.

If a client requests a certificate for site access or contract approval, make sure the certificate dates cover the period required for the work.

Do Lenders Need a Certificate of Currency?

Lenders may request a Certificate of Currency when finance is being provided for an insured asset, such as a home, vehicle, commercial property, machinery or equipment.

For home loans, a lender may ask for evidence that the property is insured before settlement. For business finance, a lender may ask for proof that financed equipment, plant, vehicles or property are insured.

The lender may also ask to be noted as an interested party. This does not automatically change the cover available under the policy. It usually confirms the lender has a financial interest in the insured asset.

When Might a Lender Not Need a Certificate of Currency?

A lender may not need a Certificate of Currency in some situations, depending on the type of property, loan or finance arrangement.

Common examples include:

- Vacant land, where there may be no building to insure

- A property under construction, where the lender may request evidence of the builder’s insurance or Contract Works Insurance instead

- Strata title units or townhouses, where the strata corporation usually arranges building insurance

Requirements vary between lenders. If the request relates to finance or settlement, the lender should confirm the exact evidence needed.

Can a Lender Ask for Strata Insurance?

Yes, a lender can ask for evidence of strata insurance. This is more common where the property is a unit, apartment or townhouse covered under a strata building insurance policy.

In many strata arrangements, the building insurance is arranged by the strata corporation rather than the individual unit owner. If a lender asks for proof of strata insurance, the strata manager can usually provide the relevant certificate or policy summary.

Unit owners may still need to consider their own contents, landlord or business-related insurance depending on how the property is used. The strata insurance policy will not necessarily cover every personal, business or liability exposure connected to the unit owner.

What Should You Check Before Sending a Certificate of Currency?

Before sending a Certificate of Currency to a client, builder, lender or contractor, check that the document matches the request.

Review the following details:

- The insured name matches your legal business name or trading name

- The policy type matches what the client requested

- The expiry date covers the required work period

- The cover limit meets the contract or site access requirement

- The business activities shown are accurate

- The interested party is listed if required and accepted by the insurer

- Any required contract wording has been reviewed by your broker or insurer

- The certificate is the latest version issued by your broker or insurer

If anything looks incorrect, contact your broker before sending the certificate. Small wording issues can delay site access, tender approval or payment processing.

How to Get a Certificate of Currency

You can usually get a Certificate of Currency from your insurance broker or insurer once the policy has been arranged and issued. In many cases, the certificate can be provided quickly after payment and insurer confirmation.

At All Trades Cover, the process is straightforward:

- Submit your details: Tell us your trade, business structure and the cover you need.

- Review your options: We compare available options from Australian trade and construction insurers.

- Choose your cover: You select the policy that suits your business, contract requirements and budget.

- Receive your documents: Once cover is arranged, your Certificate of Currency or Certificate of Insurance can be issued where available.

If you already have a policy through All Trades Cover and need a certificate for a new job, contract or site requirement, contact our team with the wording or certificate request. We can help check what can be issued under the policy.

Common Certificate of Currency Issues for Tradies and Contractors

Certificate issues often happen when contract requirements are more detailed than the policyholder expected.

Common issues include:

- The client asks for a higher Public Liability Insurance limit than the current policy provides

- The certificate does not show the exact business activity required by the contract

- The head contractor wants to be listed as an interested party

- The contract requests principal indemnity wording

- The contract requests a waiver of subrogation

- The certificate has expired before the work starts

- The policy is in the wrong business name

- The policy does not match the entity signing the contract

- The client requests cover for activities that were not disclosed when the policy was arranged

These issues can often be reviewed, but changes remain subject to insurer acceptance. It is better to raise certificate requirements before signing a contract or arriving on site.

What If a Client Rejects Your Certificate of Currency?

If a client rejects your Certificate of Currency, ask them to confirm exactly what is missing or incorrect. The issue may be simple, such as an expired certificate, or more technical, such as a contract clause that the current policy does not address.

Common reasons for rejection include:

- The policy limit is too low for the contract

- The certificate does not list the correct insured entity

- The certificate does not list the requesting party as an interested party

- The policy type does not match the contract requirement

- The certificate does not show required wording

- The business activity description is too narrow

All Trades Cover can review the request and help clarify what may be possible under the policy. Where required, we can approach the insurer to request updated wording, endorsements or policy changes. Any changes depend on insurer approval.

Frequently Asked Questions

What Is a Certificate of Currency?

A Certificate of Currency is a document confirming that an insurance policy is current at the date it is issued. It usually summarises key policy details, including the insured name, policy type, policy period and cover limit.

Is a Certificate of Currency Proof of Insurance?

Yes, a Certificate of Currency is commonly used as proof that an insurance policy is current. It is not the full policy wording and does not confirm that every possible claim or contract requirement is covered.

Who Issues a Certificate of Currency?

A Certificate of Currency is usually issued by an insurer, underwriting agency or insurance broker. If your policy was arranged through All Trades Cover, you can contact our team for certificate support.

How Quickly Can I Get a Certificate of Currency?

Timing depends on the insurer, policy type and whether the certificate needs standard or custom wording. Standard certificates can often be issued quickly once cover has been arranged and confirmed.

Does a Certificate of Currency Show What Is Covered?

A Certificate of Currency usually shows a summary of the policy type, limit and policy period. It does not list every inclusion, exclusion, condition or endorsement. The full policy wording should be checked for detailed cover information.

Can a Certificate of Currency Include an Interested Party?

Yes, an interested party can sometimes be added to a Certificate of Currency where accepted by the insurer. This is common for lenders, landlords, builders, head contractors and finance providers.

Does a Certificate of Currency Mean a Claim Will Be Paid?

No. A Certificate of Currency confirms the policy is current, but any claim is assessed against the policy terms, conditions, limits and exclusions. The insurer decides claim outcomes based on the policy wording and claim circumstances.

Can I Use an Old Certificate of Currency?

You should avoid using an old Certificate of Currency if the policy has renewed, changed, expired or been cancelled. Clients and contractors usually want the latest certificate showing the current policy period.

Do Sole Traders Need a Certificate of Currency?

Sole traders may need a Certificate of Currency when a client, builder, council, landlord or contractor requests proof of insurance. This is common for trade, construction, maintenance and service-based work.

Can All Trades Cover Help With Certificate Wording?

Yes. All Trades Cover can help review certificate requests and liaise with insurers where specific wording is needed. Any wording changes or endorsements remain subject to insurer approval.

Need a Certificate of Currency for a Job or Contract?

If you need insurance arranged or a Certificate of Currency issued for a site, tender, contract or client request, All Trades Cover can help you understand what information is needed and what may be available under the policy.

Contact All Trades Cover to discuss your insurance requirements, request a Public Liability Insurance quote or speak with our team about business insurance documents for your trade or contractor work.

General Advice Warning: This information is general only and does not take into account your objectives, financial situation or needs. Cover is subject to policy terms, conditions, limits, exclusions and insurer acceptance. Before deciding whether a policy is suitable, read the relevant policy wording and consider whether the cover meets your circumstances.