Updated July 2026

A sole trader who works alone generally does not need Workers Compensation Insurance for themselves. However, a sole trader may need Workers Compensation Insurance as soon as the business employs someone who meets the legal definition of a worker.

That can include full-time, part-time and casual employees. Some contractors and subcontractors may also be treated as workers depending on how the working arrangement is structured.

Quick summary

- A sole trader working alone generally cannot cover themselves as an employee under Workers Compensation Insurance.

- Workers Compensation Insurance may be required when a sole trader employs an apprentice, casual, part-time employee or another person who meets the legal definition of a worker.

- Having an ABN does not automatically mean a contractor falls outside workers compensation laws.

- Personal Accident and Illness Insurance may provide an alternative form of financial support for a sole trader who cannot work because of an accepted injury or illness claim.

- All Trades Cover can arrange Workers Compensation Insurance in Western Australia only due to licensing restrictions.

- Workers compensation requirements differ between Australian states and territories, so businesses operating outside WA should check with the relevant state or territory authority.

This information is general only and does not take into account your objectives, financial situation or needs. Workers compensation obligations depend on the applicable legislation, the location of the work and the actual working arrangement.

What Is Workers Compensation Insurance?

Workers Compensation Insurance is insurance that may respond when a worker suffers an injury or illness arising from their employment.

Depending on the applicable workers compensation scheme and the circumstances of an accepted claim, benefits may include:

- Compensation for a portion of lost wages.

- Reasonable medical and treatment expenses.

- Workplace rehabilitation and return-to-work support.

- Other statutory benefits available under the relevant scheme.

In Western Australia, employers must hold a current Workers Compensation Insurance policy for anyone they employ who is legally defined as a worker under the Workers Compensation and Injury Management Act 2023.

Cover and claim outcomes remain subject to the legislation, policy terms, conditions, limits, exclusions and insurer acceptance.

Does a Sole Trader Working Alone Need Workers Compensation Insurance?

A sole trader who has no workers generally does not need Workers Compensation Insurance for themselves. A sole trader is not usually treated as an employee of their own sole trader business.

This also means Workers Compensation Insurance generally does not provide personal injury or income cover for the sole trader.

A sole trader may instead consider Personal Accident and Illness Insurance. Depending on the policy selected and the circumstances of an accepted claim, Personal Accident and Illness Insurance may provide weekly benefits or other financial support when an injury or illness prevents the insured person from working.

Personal Accident and Illness Insurance is not the same as Workers Compensation Insurance. Waiting periods, benefit periods, covered events, pre-existing condition provisions and other exclusions can apply.

This table provides a general guide only. Worker definitions and insurance obligations vary between jurisdictions.

When Does a Sole Trader Need Workers Compensation Insurance?

A sole trader may need Workers Compensation Insurance when the business starts employing another person who falls within the relevant legal definition of a worker.

Hiring an apprentice

An apprentice will generally be treated as a worker. A sole trader should check and arrange the required Workers Compensation Insurance before the apprentice starts work.

Hiring a casual or part-time employee

Casual and part-time employees can fall within workers compensation laws. The fact that someone works limited hours or only helps during busy periods does not necessarily remove the employer’s insurance obligation.

Hiring administrative or office support

Workers compensation obligations are not limited to people working on tools or construction sites. An office administrator, scheduler or other support employee may also need to be included.

Engaging contractors or subcontractors

A contractor or subcontractor may be treated as a worker in some circumstances. An ABN, invoice or contractor agreement does not settle the question by itself.

Do Subcontractors Need to Be Included in Workers Compensation Insurance?

Some subcontractors may need to be included, depending on the law and the way the work is actually performed.

In Western Australia, a contractor or subcontractor may fall within the definition of a worker where the arrangement involves the person providing personal manual labour or services for another business. Principal and contractor obligations may also arise within contracting chains.

Relevant factors may include:

- Whether the person is mainly paid for their own labour or services.

- Who controls when, where and how the work is completed.

- Whether the person can delegate or subcontract the work.

- Who supplies the tools, equipment, vehicles or materials.

- Whether the person works independently or as part of the business’s usual operations.

- Whether the person carries the commercial risk of completing the work.

No single factor determines the result in every case. The written agreement and the practical working relationship should be considered together.

WA businesses can review the current WorkCover WA guidance for contractors and subcontractors. Businesses should seek independent legal or regulatory guidance where the worker classification remains unclear.

Workers Compensation Requirements in Western Australia

In Western Australia, an employer must hold Workers Compensation Insurance for anyone the Workers Compensation and Injury Management Act 2023 defines as a worker.

The definition can include:

- Full-time employees.

- Part-time employees.

- Casual and seasonal employees.

- Piece-rate and commission workers.

- Some working directors.

- Some contractors and subcontractors.

WorkCover WA administers the workers compensation scheme in Western Australia. Employers can review their obligations through the WorkCover WA guidance on covering workers.

All Trades Cover can arrange Workers Compensation Insurance in Western Australia only due to licensing restrictions. For workers compensation requirements in another state or territory, contact the relevant local authority:

- Australian Capital Territory: WorkSafe ACT.

- New South Wales: State Insurance Regulatory Authority.

- Northern Territory: NT WorkSafe.

- Queensland: WorkCover Queensland.

- South Australia: ReturnToWorkSA.

- Tasmania: WorkSafe Tasmania.

- Victoria: WorkSafe Victoria.

- Western Australia: WorkCover WA.

Requirements and scheme arrangements may change. Check the relevant authority’s current guidance before hiring workers or starting work in another jurisdiction.

Workers Compensation vs Public Liability vs Personal Accident Insurance

Workers Compensation Insurance, Public Liability Insurance and Personal Accident and Illness Insurance address different types of risk. One policy does not automatically replace another.

Public Liability Insurance

May respond to certain claims involving third-party personal injury or property damage arising from the insured business activities.

General focus: Injury or damage involving other people and their property.

Workers Compensation Insurance

May provide statutory benefits when a legally defined worker suffers an accepted work-related injury or illness.

General focus: Work-related injury or illness affecting workers.

Personal Accident and Illness Insurance

May provide agreed benefits to the insured person following an accepted injury or illness claim, subject to the selected policy.

General focus: The sole trader’s own ability to work and earn an income.

For example, a sole trader working alone may consider both Public Liability Insurance and Personal Accident and Illness Insurance. If the business later employs a worker, Workers Compensation Insurance may also become necessary.

Public Liability Insurance generally does not replace Workers Compensation Insurance. Personal Accident and Illness Insurance also does not remove an employer’s statutory obligation to insure eligible workers.

Each form of cover is subject to its own policy terms, conditions, limits, exclusions and insurer acceptance.

What Could Happen If an Employer Does Not Hold Required Cover?

An employer that does not hold required Workers Compensation Insurance may face financial and regulatory consequences.

Depending on the jurisdiction and circumstances, consequences may include:

- Penalties for failing to hold compulsory insurance.

- Liability for compensation or statutory claim costs.

- Recovery action by the relevant workers compensation authority or insurer.

- Delays while the worker’s status and the employer’s obligations are assessed.

- Contract or site-access issues where evidence of insurance is required.

The exact consequences depend on the applicable legislation. Businesses should not assume that a worker falls outside the scheme simply because the arrangement is temporary or described as subcontracting.

Examples of When the Answer May Change

The following examples show how a sole trader’s workers compensation obligations may change. They are general illustrations only and do not indicate that a claim would automatically be accepted.

A sole trader hires an apprentice

A self-employed builder begins employing an apprentice. The builder may now have an obligation to arrange Workers Compensation Insurance before the apprentice starts, even though the business previously operated without employees.

A contractor brings in casual labour

An earthmoving contractor hires a casual labourer for several days of site work. Short-term employment can still create workers compensation obligations.

A regular subcontractor works as part of the business

A welding business regularly engages the same individual to provide personal labour under the business’s direction. The individual may be treated as a worker despite holding an ABN and submitting invoices.

A sole trader is injured while working alone

A self-employed plumber who has no workers suffers an injury and cannot work. Workers Compensation Insurance would generally not cover the sole trader as their own employee. A Personal Accident and Illness Insurance policy may respond where the event is covered and the claim is accepted.

When Should a Sole Trader Review Their Insurance?

A sole trader should review their insurance whenever the way the business operates changes.

Review your setup when you:

✓ Hire your first employee or apprentice.

✓ Start using casual or seasonal labour.

✓ Engage regular subcontractors.

✓ Change how contractors are supervised or paid.

✓ Begin operating in another state or territory.

✓ Add a new company, trust or employing entity.

✓ Increase or reduce your estimated wages.

✓ Take on contracts with new insurance conditions.

Workers Compensation Insurance premiums commonly use information such as the business’s industry classification and estimated wages. Changes should be reported to the insurer or broker so the policy records can be reviewed.

How All Trades Cover May Be Able to Help

All Trades Cover is a specialist insurance brokerage for trades, construction, mining and heavy industry. Our brokers can help WA sole traders and employers understand the information insurers require and compare available Workers Compensation Insurance options.

Depending on your circumstances and insurer acceptance, our team may be able to help with:

- Reviewing your business structure and the workers you engage.

- Explaining the information required for a Workers Compensation Insurance application.

- Arranging Workers Compensation Insurance for eligible WA businesses.

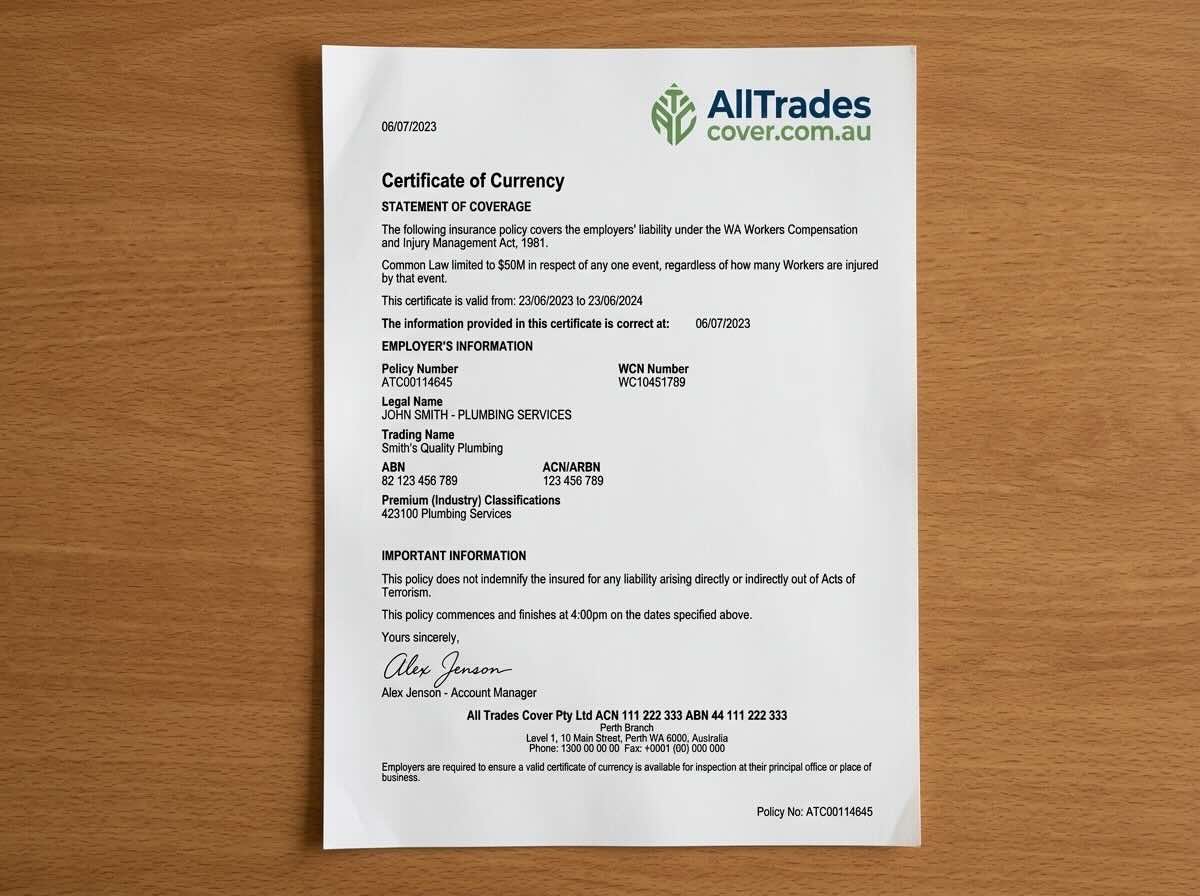

- Coordinating policy documents and Certificates of Currency.

- Updating policy details when wages, workers or business activities change.

- Supporting clients through the claims process without controlling the insurer’s claim decision.

All Trades Cover holds Australian Financial Services Licence 418512. Workers Compensation Insurance can only be offered by All Trades Cover in Western Australia due to licensing restrictions.

To discuss your WA business setup, contact All Trades Cover or request information about Workers Compensation Insurance.

Cover is subject to policy terms, conditions, limits, exclusions and insurer acceptance. All Trades Cover can provide general information and insurance broking services but does not determine whether a person is legally a worker or whether a claim will be accepted.

Frequently Asked Questions

Do I need Workers Compensation Insurance if I only hire someone occasionally?

You may still need Workers Compensation Insurance. A person can be a worker even when they are employed casually, temporarily or for only a small number of hours. Check the definition of a worker in your state or territory before the person starts.

Can a sole trader get Workers Compensation Insurance for themselves?

A sole trader generally cannot insure themselves as an employee of their own sole trader business. Personal Accident and Illness Insurance may provide an alternative, subject to the policy terms, covered events, waiting periods, benefit limits, exclusions and insurer acceptance.

Does an ABN mean someone is not a worker?

No. An ABN is only one part of the arrangement. A contractor or subcontractor may still be legally treated as a worker depending on the services provided and how the work is carried out.

Do apprentices need Workers Compensation Insurance?

Apprentices will generally need to be covered as workers. A sole trader taking on an apprentice should confirm the applicable insurance requirements before the apprenticeship or employment begins.

Does Public Liability Insurance cover injuries to employees?

Public Liability Insurance generally excludes injury to employees where workers compensation laws apply. Workers Compensation Insurance and Public Liability Insurance address different liabilities and may both be required.

Can Personal Accident Insurance replace Workers Compensation Insurance?

No. Personal Accident and Illness Insurance does not replace an employer’s legal obligation to hold Workers Compensation Insurance for eligible workers. Personal Accident and Illness Insurance is commonly considered by sole traders seeking cover for their own inability to work.

What happens if a worker is injured away from the main worksite?

An injury away from the usual worksite may still be work-related, depending on what the person was doing and the connection between the activity and their employment. The insurer assesses each claim using the relevant legislation and evidence.

Do I need to update my policy if my wages change?

You should tell your insurer or broker when your estimated wages or workforce change. Workers compensation premiums can be adjusted using declared and actual wage information, subject to the scheme and insurer requirements.

Is Workers Compensation Insurance tax deductible?

Workers compensation premiums paid for business purposes may generally be treated as a business expense, but the tax treatment depends on your circumstances. Confirm the treatment with a registered tax agent or accountant.

Can All Trades Cover arrange Workers Compensation Insurance outside WA?

No. All Trades Cover can only offer Workers Compensation Insurance in Western Australia due to licensing restrictions. Businesses in other states and territories should contact the relevant workers compensation authority or an appropriately licensed provider.

Who decides whether my subcontractor is a worker?

The legal position depends on the relevant workers compensation legislation and the actual working arrangement. An insurer, workers compensation authority, tribunal or court may assess the arrangement where the classification is disputed. A broker can help gather insurance information but cannot make a binding legal determination.

This information is general only and does not take into account your objectives, financial situation or needs. Workers compensation laws and scheme requirements vary between Australian states and territories and may change. Check the current requirements with the relevant regulator and seek independent legal, tax or financial advice where required. Cover is subject to policy terms, conditions, limits, exclusions and insurer acceptance.